CIBIL Deciphered: Why Your Credit Score is Your Financial Identity

Understand why 3 digits determine your financial future. Learn how Credit Reporting Agencies work and how to leverage your score for better loans.

In the physical world, your identity is defined by your name and your face. In the financial world, those things matter very little. To a bank, you are primarily a three digit number between 300 and 900. This is your credit score, and it is the most influential data point in your life.

It acts as a digital resume that tells every lender in the country exactly how much they can trust you before you even say hello. Most people treat their credit score as a vague exam result they check once a year. In reality, it is a living, breathing reflection of your financial integrity.

The Invisible Observers: Credit Reporting Agencies

Before we look at the number, we have to look at who is watching. In India, there are four major Credit Reporting Agencies: CIBIL , Experian , Equifax , and CRIF High Mark . These companies are the librarians of your financial life. They do not lend money; they simply collect data from every bank you have ever interacted with.

While you might hear people say “ Check your CIBIL ”, they are usually referring to your credit report in general. CIBIL is simply the oldest and most widely used agency in India. Every time you open a card, miss a payment, or even just inquire about a loan, these agencies take a note. Your credit score is the final grade they give you based on those notes.

The Gatekeeper of Your Future Goals

Think of your credit score as the ultimate gatekeeper. When you apply for a home loan, the bank does not just look at your current salary; they look at your history of keeping promises. A high score (typically 750+) signals that you are a low risk bet. This trust translates into tangible power: lower interest rates and faster approvals.

A difference of just 1% in a home loan interest rate, triggered by a mediocre score, can cost you tens of lakhs of rupees over 20 years. In this light, a poor score is not just a bad grade; it is a massive, invisible tax on your future self. It determines whether you get the keys to your first home or remain stuck in the waiting room.

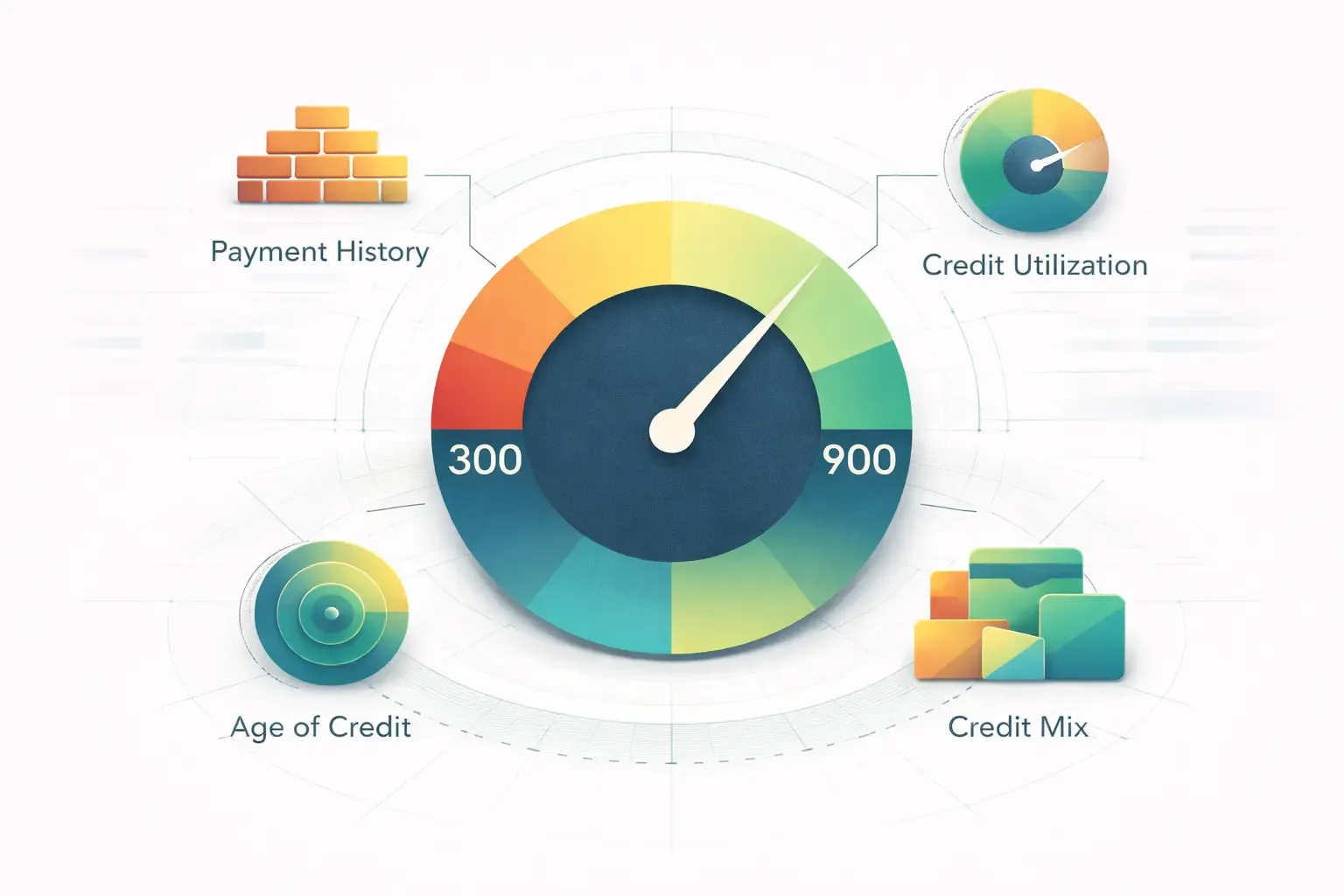

The Anatomy of the 3-Digit Number

Your score is not generated by magic; it is a cold, hard calculation based on your behavior. The biggest factor is your Payment History. Every time you pay a bill on time, you add a brick to your wall of credibility. One single missed payment, however, can act like a sledgehammer, knocking your score down by points that take months to recover.

The second major factor is Credit Utilization. Banks look at how much of your total limit you actually use. If you have a limit of ₹1 Lakh and you consistently spend ₹90,000, you look credit hungry and desperate, which scares lenders. The philosophy for a perfect score is simple: keep your utilization below 30%. It shows you have the power to spend, but the discipline not to.

Why “No Credit” is Not “Good Credit”

A common mistake is believing that avoiding credit cards entirely will keep your financial identity clean. This is a myth. If you have never borrowed money, you have no credit history. To a bank, a person with no history is almost as risky as a person with a bad one. Without data, the bank has no way to predict if you will pay them back.

This is why a credit card is the most effective tool for building a financial identity. By using a card for small, planned expenses and paying it off in full, you are essentially interviewing for your future home loan every single month. You are proving, in real time, that you are a person of your word.

Choosing Your Reputation

This three-digit number is fragile and requires constant monitoring. Identity theft, reporting errors by banks, or even an old forgotten card with a small pending fee can tank your score without you realizing it. Checking your report regularly is not paranoia; it is reputation management.

Your credit score is the price you pay for the trust you haven’t earned yet.

In the Zero Interest philosophy, we do not just build credit for the sake of cards; we build it so that when life’s big moments arrive, the gatekeeper opens the door without hesitation. You are not just managing a number; you are managing your freedom.